How did the Spanish public administrations reduce their deficit?

The Spanish central government based its fiscal adjustment on obtaining new revenues through tax increases while the autonomous communities reduced their expenditure by 14%

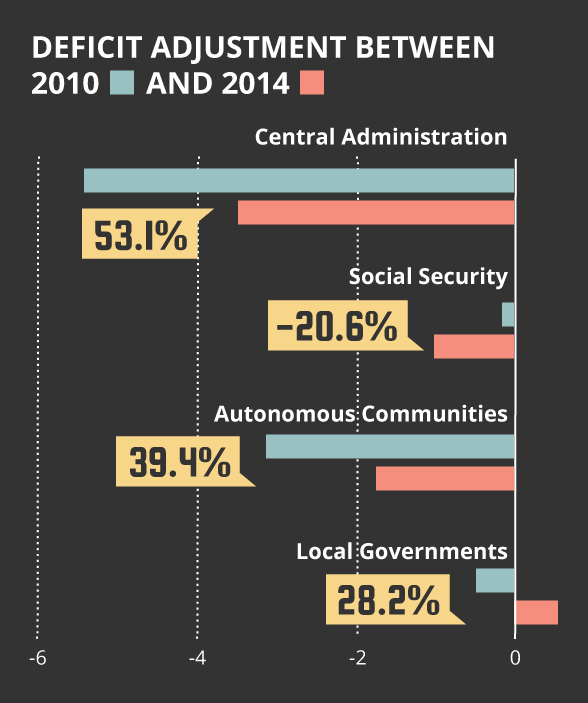

Between 2010 and 2014, the Spanish public administration as a whole -central government, social security, autonomous communities and local governments- successfully reduced its deficit by 3.57 points, from 9.35% to 5.78% of GDP.

Public administrations may carry out fiscal consolidation processes through the implementation of measures having an impact on revenue or expenditure, or simultaneously on both. The choice of instrument is determined by each administration's capacity to increase its revenue and/or curb its expenditure. In this regard, an analysis of deficit adjustments achieved by each of the Spanish public administrations shows that their fiscal consolidation processes have been of a very different nature.

Spanish central government: adjustment through taxes

The Spanish central government controls almost all taxes paid by citizens, which allows for tax increases whenever revenue is needed. This is precisely what the central government did during the worst years of the crisis: between 2010 and 2014, successive increments of VAT, PIT (Personal Income Tax) and excises enabled the central government to collect over 25 additional billion euro throughout Spain.

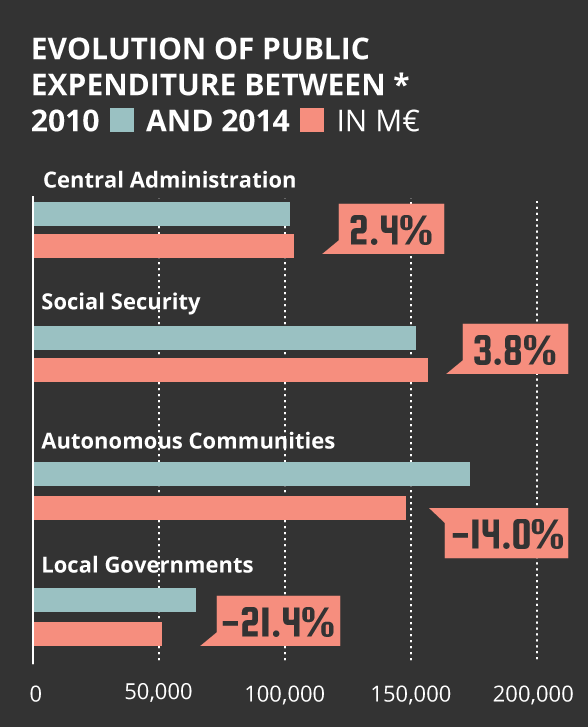

Thanks to this increase in tax collection, the central government was able to make an adjustment of 21.7 billion euro between 2010 and 2014, thus reducing its deficit from 5.43% to 3.56%. Furthermore, all this was possible without a contraction in expenditure, which actually increased by 2.4%.

Despite the fact that under the current financing model VAT, PIT and excises are taxes shared with the autonomous communities belonging to the common system , the general government did not transfer them any proportion of these 25 additional billion collected between 2010 and 2014. What is more, tax increases approved by the central government have led to an increase in the territorial governments' current expenditure, with an impact of about 200 million euro on the Generalitat of Catalonia.

Social Security: deficit increases

As far as the Social Security is concerned, in the period 2010-2014 the performance of both revenues and expenditures had a negative impact on deficit, which increased by 8.4 billion euro (from -0.23% in 2010 to -1.04% in 2014). This performance is explained by labour market developments, which lead to a decrease in revenue -due to the loss of income collected through social contributions- and an increase in expenditure, which was under strong pressure because of an increase in unemployment. In fact, expenditure rose by 3.8% between 2010 and 2014.

Autonomous Communities: adjustment through expenditure

Unlike for the central government, the tax bases for the autonomous communities are very narrow. Therefore, there is little scope for raising revenue through higher taxes. Some autonomous communities have created their own taxes, increased certain tax rates or resorted to the sale of real property assets. However, notwithstanding the adopted measures, revenue for the autonomous communities as a whole during the period 2010-2014 decreased by approximately 1%. It should be noted that the tax on capital transfers and documented legal acts, one of the regionally managed taxes providing the highest revenues, is closely linked to the real estate business, where collections have decreased substantially following the crisis.

Given the difficulties to increase revenues, the fiscal consolidation process in the autonomous communities has focused mainly on adjusting expenditures, which fell by 14% between 2010 and 2014. The overall deficit in the autonomous communities declined by 1.43 points, from -3.17% in 2010 to -1.75% in 2014. It is important to remember that over 70% of total expenditures by the autonomous communities are used to provide citizens with health, education and welfare services, since these competences have been transferred to them.

For more information about the composition of expenditures by the autonomous communities, please refer to Annex 1 to this article.

Local governments: adjustment through revenues and expenditures

The fiscal consolidation process in the local governments combines a huge expenditure reduction effort -21% adjustment in the period 2010-2014- and an increase in revenues through tax increases, namely of the real estate tax. This allowed the local governments as a whole to reach an overall adjustment of 11.5 billion euro, from a deficit of 0.52% of GDP in 2010 to a 0.57% surplus in 2014.

Last March 31st the Ministry of Finance and Public Administrations of the Spanish Government reported the provisional outturn for year 2015. Spain's 2015 deficit came in at 5.16% of GDP. Deficits for central government, social security and autonomous communities were 2.58%, 1.26% and 1.66% respectively, while local governments recorded a surplus of 0.44%. Consolidated data on revenue and expenditure are not still available.

1Even though there are 17 autonomous communities in the Spanish State, the financing model is applied only to 15 communities, as the Basque Country and Navarre have a separate regime.

Source: State Government Comptroller's Office (IGAE) + own elaboration

State Government Comptroller's Office (IGAE)

(*) Consolidated amounts. Excluding internal transfers for all subsectors and consolidated interests for the central government.